I like to start conversations about the future with this Chinese proverb: “When the winds of change blow, some build walls while others build windmills.”

Are you building walls while the world changes around you? Or are you building windmills?

While change often comes slowly to agriculture, it will come. We need to be prepared for it. The global research team at CHS sees several drivers to watch as you execute on your business strategy over the next five years. Here’s six trends to watch.

1. Outside forces matter

Agriculture is not insulated from what’s happening in the broader world, so we need to pay attention to outside forces at work.

U.S. economics were relatively quiet for a long time after the recession of 2008-2009. In fact, I would say we had 15 years of a strong bull run:

- Equities markets rose steadily and considerably. That put money in pockets and fueled 401(k) plans.

- Unemployment declined to record lows.

- Interest rates were near zero, thanks to federal monetary policies.

Fast-forward to today and we are in the midst of spiking inflation and broad market concerns over Federal Reserve restrictive actions to control it. These swift-moving macroeconomic forces have quickly spilled into other markets, including commodities.

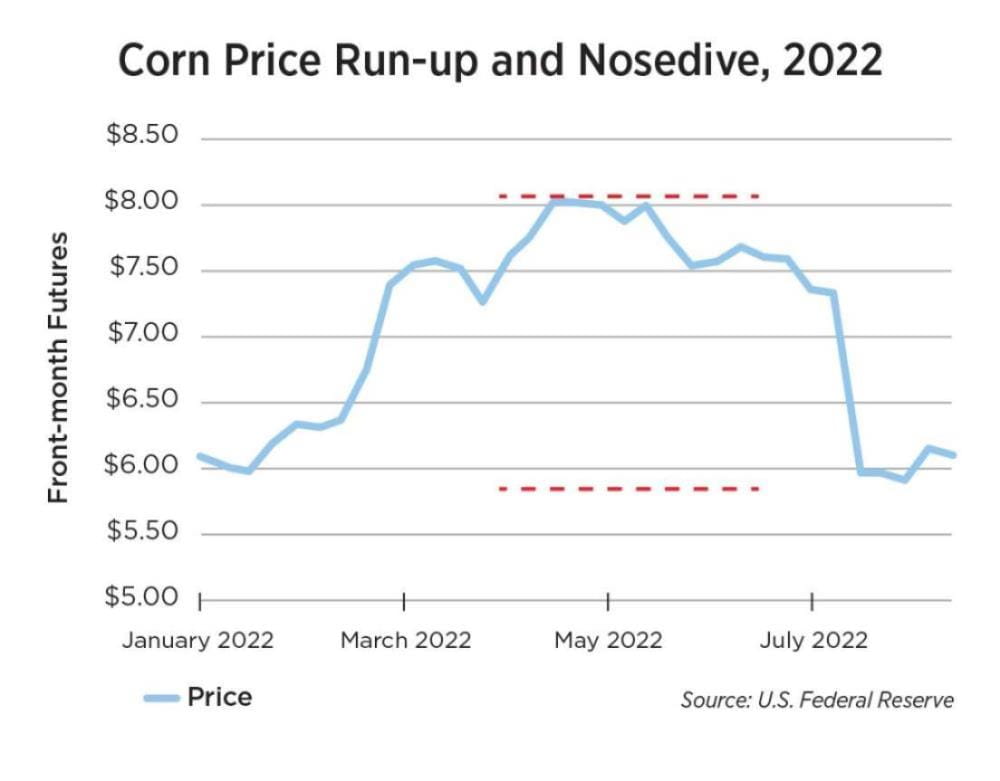

In early 2022, as the Federal Reserve began to pursue rate hikes, equities markets went “risk off,” backing away from markets and taking commodities with them. As a result, corn moved from more than $8 per bushel to roughly $6 per bushel in a few months. The typical fundamental drivers that influence ag prices — planting progress, weather, etc. — didn’t matter.

Bottom line: The trillion-dollar equities markets trumped the billion-dollar commodities markets, proving ag commodities are not insulated from outside economic forces. While the impact of markets outside of commodities was largely muted before 2021, we can’t afford to ignore them in the current economic environment.

2. Labor market upset

Labor will continue to be a hot topic in agriculture and globally. We have seen three major drivers behind limited U.S. labor availability:

- When the pandemic hit, baby boomers tapped out of the labor market, taking more than 3 million people out of the workforce.

- Between 1 million and 2 million people of prime working age (25 to 54) dropped out of the workforce to care for family members during the pandemic.

- Immigration reform in 2016 made it difficult for new workers to enter the country to meet labor demand.

For those still working, expectations have changed, as noted in a recent McKinsey & Company study. What used to be important to traditional workers — career advancement and development, compensation, meaningful work — is less important to newer employees. Those new workers rate workplace flexibility at the top of their wish list, followed by compensation, meaningful work and support for health and well-being.

As we think about attracting and retaining talent for agriculture, the rules have changed. Members of the latest generation to enter the workforce — often called Gen Z — are tech-savvy, have a do-it-yourself (DIY) mentality and are highly competitive. They want a say in decision-making — after all, they grew up having a say in family decisions — and they demand career pathways and details on where they’re going and how they’ll get there.

3. Supply shifts

Crop input prices and, perhaps just as important, availability will continue as a key theme in agriculture.

On the crop protection side, most active ingredients now come from China and are subject to what’s going on in that country in terms of both production and demand. Supply chain upsets, both current and future, will impact how much product is delivered to U.S. agriculture and at what price.

Crop nutrient production is another global industry, although the U.S. is a fairly significant fertilizer producer, providing about 15% of the world’s total fertilizer production. Unfortunately, our demand is greater than our production, so we are subject to global trade and competition for products.

While we import crop nutrients from Canada, much also comes from the Middle East and North Africa — that’s where normally cheap natural gas feedstocks for fertilizer production are available to help us close the demand gap.

All these market and industry factors combine to impact U.S. crop producers through volatile, if not increased, production costs.

Iowa State University researchers say soybean input costs rose 15% and corn input costs rose about 20% in 2022 — and fertilizer costs were 23% of corn production costs and 15% of soybean costs. With the renewable diesel movement and the cost to grow the crop, do you switch from corn to soybeans?

We’ll need to gain efficiencies. Those could come from application technology advances like spot spraying or from genetic shifts like short corn that reduce nitrogen and crop protection needs and make the crop more resilient to volatile weather.

4. Renewable diesel renaissance

It is rare to have a new source of demand in the commodities world. Lightning already struck once for agriculture in the mid-2000s with ethanol as a fuel oxygenate and additive for gasoline. It’s about to strike a second time with soybeans and renewable diesel.

Today, U.S. farmers produce 15 billion bushels of corn every year and 5 billion bushels go into ethanol, fully one-third of our corn production. But is the ethanol arc waning?

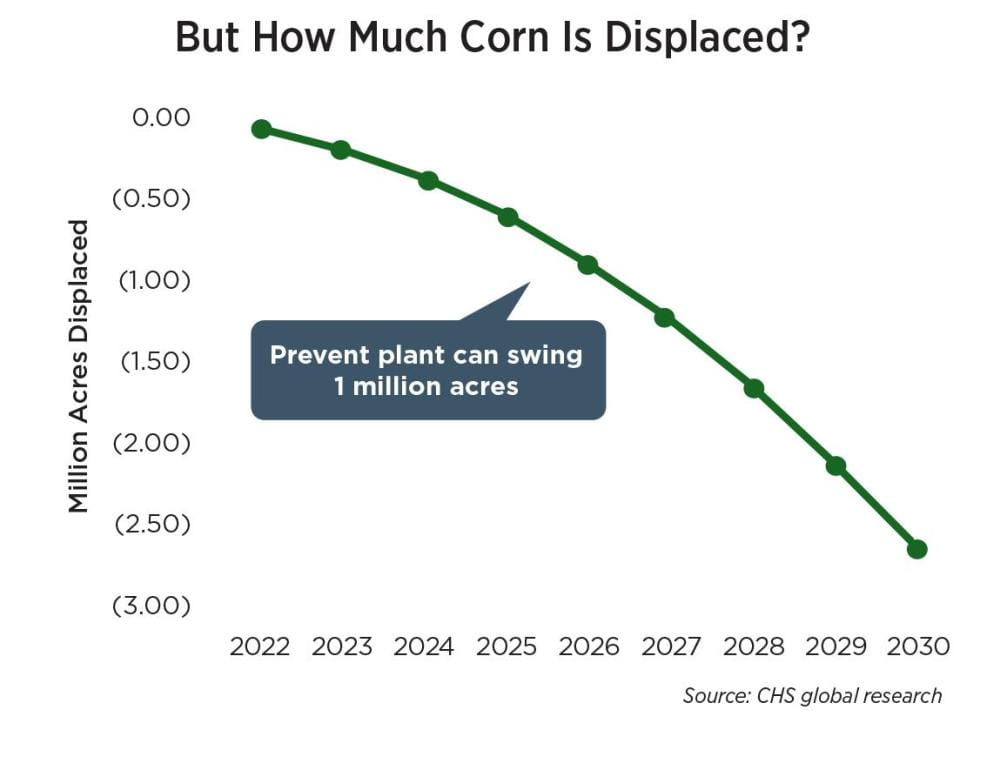

In 2022, there were more than 50,000 electric vehicle (EV) charging stations in the U.S. — nearly 12 times the number of E85 stations, according to the U.S. Department of Energy. Federal government and industry predictions say we could have 25 million new EVs on the ground by 2030, or about 30% of all new car sales.

How much corn would be displaced if EVs rise as predicted and gas and ethanol demand decreases? Figure 25 million cars at 550 gallons of fuel per year, with 10% of the fuel being ethanol. That displaces 2 million to 2.5 million acres of corn. That much decline can happen from prevented planting in one or two states in any year!

While EVs will continue grabbing headlines, there will still be demand for corn. And that’s not taking into account the impact of potentially moving to E15 blends or sustainable aviation fuel, which is derived from ethanol. In short, corn demand is not going away any time soon.

Soybean markets are responding to renewable diesel demand fueled by low-carbon fuel standards. If you total up the expanded soy crush capacity being built now, we’ll need 9 million to 11 million or more additional soybean acres to satisfy the demand.

Where will all those beans come from? We export roughly half of the beans we produce in the U.S. today, so you can anticipate many of those acres being tipped back toward domestic demand. And the soy crush byproduct is no longer soybean oil; longer term, we’ll have to figure out what to do with all the soybean meal.

5. Deglobalization changes the game

This might be the most important factor to affect agriculture long term: a transition away from a global world order toward deglobalization. Four countries matter significantly in agriculture, and their actions will determine what happens next.

A major exporter of corn and soybeans, the United States has long enjoyed effective infrastructure to get crops from the country’s interior to the coasts. We are ag tech innovators and leading importers of crop inputs.

Watch for continued focus on exports, as well as reimagining domestic energy production through use of feedstocks like soybean oil. This may result in a pivot of soybeans from export to domestic consumption. Conversely, long-term buyers of soybean meal will be needed.

A prolific producer of soybeans and secondarily of corn, Brazil has a lot of land and isn’t afraid to convert it to ag uses, including for industrial-scale farming with farms of 5,000 to 10,000 acres or more.

According to the most recent Brazilian ag census in 2017, at that point, the country already had more than 51,000 farms with more than 1,000 hectares (2,470 acres). While soybean production in South America has continued to grow, weather effects have reduced yield there, just as they have in North America.

Watch for continued emphasis on large-scale production and exporting core grains and oilseeds, particularly corn. With deglobalization comes the opportunity for bilateral trade agreements like the recent announcement that China will accept Brazilian corn. But also be mindful of currency fluctuations between the U.S. dollar and Brazilian currency, which could have a significant impact.

China is a demand sink for all commodities. Its increasingly industrial livestock sector is shifting rations and that is changing demand for soybeans, soybean meal and corn. China is also a key producer of fertilizer and crop protection ingredients, which the U.S. needs.

Watch for China’s commitment to its five-year plan and the country’s changing demographics. China has committed to expanding agriculture with the goal of being self-sufficient.

According to the U.S. Census Bureau International Database, by 2030, more people in China will be over 65 years old than are under 15 years old. That will likely create a tipping point for commodity demand, if it hasn’t already happened.

Much of the world’s wheat is grown in Russia and Ukraine and we expect that to continue. Those countries are key to fertilizer trade and are big players in energy. Because their production has to flow in and out of the Black Sea, they have less access to ocean transportation than we have in the U.S.

Watch for continued difficulty in market access and potentially crop production as the Russian war in Ukraine continues.

Global markets and geopolitical situations change every day, so you need to keep them in mind as you work your plan through annual cycles. Tomorrow won’t be the same as today, so lean into change and make it work for you.

6. Technology advances in agriculture

Technology continues to advance how we work, and agriculture is not immune to those advances. Viewing and embracing technology as a competitive advantage versus simply a cost of doing business will continue to propel the most successful enterprises.

Key developments driving technological change in agriculture include:

Robotic process automation (RPA)

RPAs are essentially robots loaded onto computer systems to do repetitive transactional work. Anything a human can do with a computer, an RPA — or bot — can execute, including things like processing emails and preparing invoices. This type of efficiency may help offset current and pending labor shortages.

Drones

You’ve probably seen drones doing agronomic scouting. They can also measure volumes of grain or count livestock and other inventories. Drones are being used at CHS to inspect elevators and other facilities, which improves safety by keeping people off scaffolds and elevators.

Autonomous vehicles

According to the American Trucking Associations, we will have a shortage of 160,000 truck drivers by 2031. As an industry, we will be forced to look at technologies that will help us fill that gap from an efficiency standpoint and safety perspective. Autonomous tractors have been launched and retailers like Walmart are testing autonomous delivery vehicles between distribution centers and retail stores.

The time to embrace technology is now — it will transform the industry but requires focus and investment if we are going to use technology to meet the challenges we face.