One of the interesting things about heading into an inflationary environment is that an entire generation of farmers has never experienced anything like what we’re seeing now. They haven’t had to learn how to manage their operation differently to account for a double-digit interest environment. Even for farmers who have lived through times of high inflation, it’s hard to draw comparisons to the past. Current price levels are historic — we haven’t seen anything like this. There are so many dynamics, from labor shortages to supply chain issues, and it’s hard to separate one factor from another. The war in Ukraine has made the global supply and demand situation even more uncertain.

With all this uncertainty, consumers and producers are hearing a variety of advice and analysis. Here are some myths floating around right now.

Myth #1: Exports increase when currency is devalued.

A textbook would say inflation devalues a currency, which should open up more avenues for exports. When the U.S. dollar is weaker, for example, foreign currencies should be able to buy more of our goods more easily.

However, a weaker dollar today doesn’t push up commodity prices right now because the commodity trade is pretty inelastic. If the dollar index starts to go way down, it’s not as if China suddenly says, “Soybeans are on sale, so we’re going to buy 10 times more!” It just doesn’t work that way. When countries buy commodities from the U.S., everything they purchase has to go into a person or into an animal. Because that demand doesn’t change quickly, the impact on exports might be less than expected.

An example closer to home is consumers buying toilet paper. Households use a finite amount every year. If the price is a little higher or a little lower, we still buy the same amount. If it’s on sale we might buy more, but throughout the course of the year, it adds up to be roughly the same amount.

Whether we export more is a function of supply and demand in the market, not an external force like the dollar index.

Myth #2: Risk management strategies right now should revolve around prices.

With an increased inflationary environment, we generally see higher price volatility. And higher volatility leads to bigger cash flow needs. So if you have higher volatility and higher prices, margins will be higher. If you’re in the futures market, you need more cash to pay your broker for margin requirements. When we get into periods of high volatility like the one we’re in now, it’s not a matter of exactly what price you’re buying or selling at; it’s a cash flow situation. Do you have enough cash to pay your margin call?

Right now, producers should be looking at their overall profit margins rather than just high input prices. What does your operational margin look like? Are you profitable when locking in both ends of that spectrum? What are your input costs, irrigation costs and fuel costs? What does your return per acre look like? Can you make profitable decisions at those levels? It’s important to look at your whole farm operation to make the best decisions.

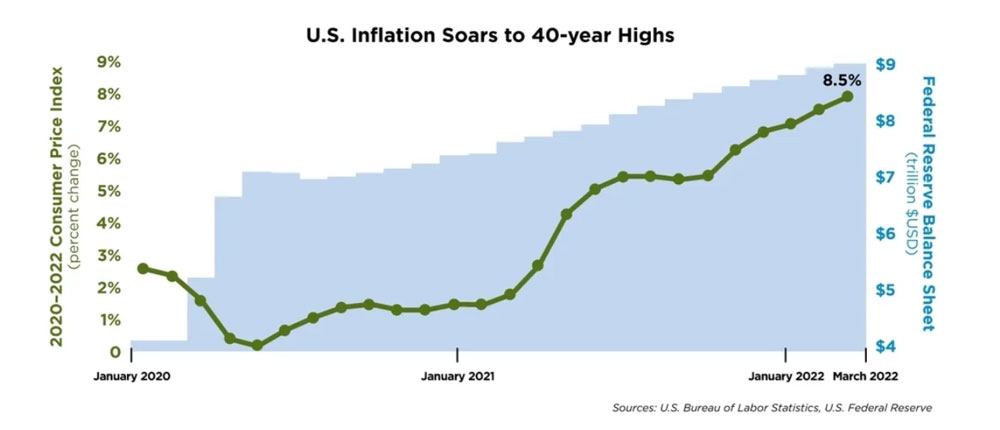

Myth #3: Inflation is temporary.

For a long time, the Federal Reserve said inflation was supposed to be transitory. The Fed isn’t using that word anymore and is rethinking how it talks about inflation.

Every three months, members of the Fed Board of Governors have an opportunity to submit forecasts on where they think interest rates are heading. The forecasts give us a sense of the sentiment held by the people who set interest rates. In the most recent report, most forecasts didn’t predict runaway interest rates — they indicated the rates will settle down. But they also think this period of higher inflation and higher interest rates will probably persist for at least two years.

Joe Lardy is a research analyst with the CHS global research team.

Related stories:

- Inflation 101: Why it’s happening and what causes it

- How today’s financial picture is rewriting the 1980s script

- 5 things to know about crop nutrient costs

Check out the full Spring 2022 issue of C magazine with this article and more.

The material provided is for informational purposes and should not be viewed as a recommendation to buy, sell or hold any commodity contract, investment or security or to engage in any risk management strategy or transaction. This information is taken from sources that we believe to be reliable, but is not guaranteed by CHS as to accuracy or completeness. The information and opinions represented are those of the author, are subject to change and may be inconsistent with the views of CHS Inc. or any of its subsidiaries.