Even as prices for crop nutrients continue to soar, growers remain engaged in the market. They have cash on hand and tell us they’re confident about what they’re growing this spring. Despite that positive sentiment, we’re keeping a careful eye on world events in our forecasting models. Consider these factors as you make decisions about crop nutrient purchases.

1. Nitrogen supply in the U.S. is adequate — for now.

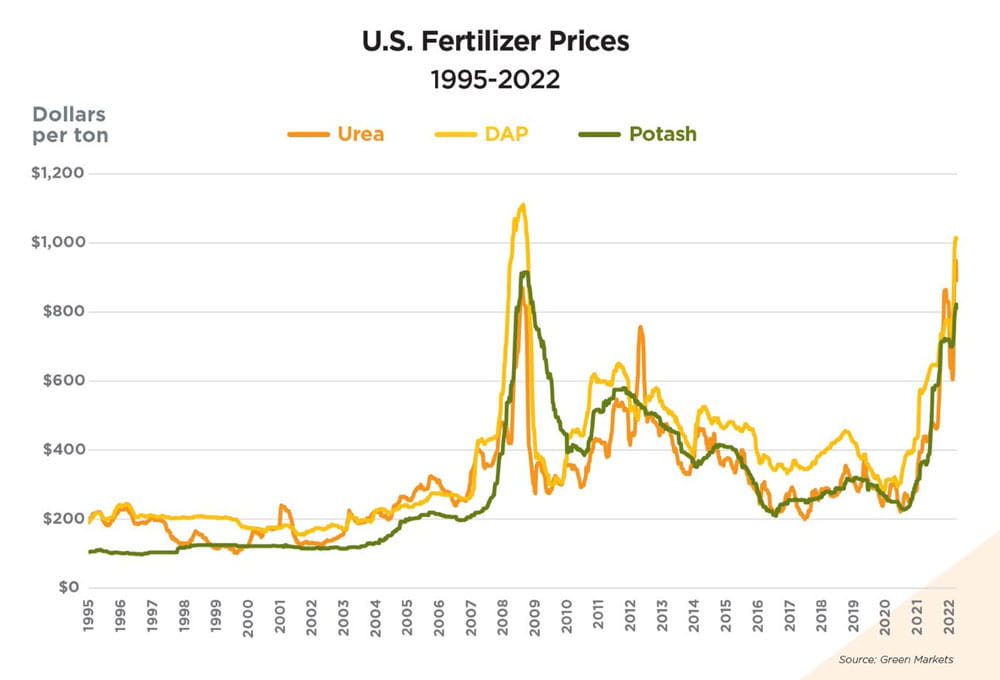

There’s plenty of nitrogen production in the United States, but we’re still seeing cost increases because U.S. prices generally follow global prices. In the U.S., we imported a lot of fertilizer before the current price run-up, so we don’t have severe fertilizer supply chain issues right now. There might be localized problems in some areas of the country, but on a macro level the U.S. is looking good.

2. Russia’s invasion of Ukraine changes the equation.

Ukraine and Russia produce and export nitrogen-based fertilizers, contributing about 20% of the global trade flow. Right now, Ukraine can’t produce fertilizer, get it to port or ship it out. We don’t know yet what the supply chain will look like later this year if we can’t source product due to this situation.

3. All ag roads lead to China.

China produces roughly 30% of the world’s urea. If 2021 urea exports from China are curtailed in 2022 and beyond, we would likely not see that product replaced in the marketplace until late 2023 as new urea manufacturing projects in areas with cheap natural gas are completed. With global demand still rising, any absence of Chinese urea will be acutely felt.

4. P and K are feeling the pressure of world events, too.

Russia and Belarus contribute over 40% of total potash trade flows, and Russia contributes almost 15% to total phosphate trade flows. Brazil imports approximately half of its fertilizer from Russia and Belarus — and the premiums Brazil buyers are paying for potash and phosphate over U.S. gulf prices is in the unheard-of $200 to $300 per ton range.

5. Uncertainty makes it hard to forecast 2023.

There’s a lot of interest right now in 2023, but the volatility we’ve seen recently has been a challenge for our pricing models. The models have never seen input prices like these. Our models are not pointing to much relief in fertilizer prices for the next year, and with 2023 new-crop grain prices well under 2022 prices, we’re in a new world.

Matt Welp is an agronomy research analyst for the CHS global research team.

Learn more about agricultural inflation:

- Inflation 101: why it’s happening and what causes it

- Three myths about ag inflation

- How today's financial picture is rewriting the 1980s script

Check out the full Spring 2022 issue of C magazine with this article and more.

The material provided is for informational purposes and should not be viewed as a recommendation to buy, sell or hold any commodity contract, investment or security or to engage in any risk management strategy or transaction. This information is taken from sources that we believe to be reliable, but is not guaranteed by CHS as to accuracy or completeness. The information and opinions represented are those of the author, are subject to change and may be inconsistent with the views of CHS Inc. or any of its subsidiaries.